If you’re considering doing an M&A deal, you’ve probably heard this advice: make sure your offer is 100% cash. Equity is a lottery ticket. Cash in your pocket is cash in your pocket.

You’ve also probably heard the horror stories of equity deals. Someone works for years — maybe even decades — on a business. They sell it for millions, on paper anyway. But because of the legal implications in the transaction documents, they only end up with a fraction of the purchase price.

Taking cash in a deal isn’t bad advice, and those stories are real. But I don’t think it’s the best perspective. And certainly isn’t the best perspective for every entrepreneur.

Let me tell another story. You work on your SaaS business for years. It’s growing. You decide to take advantage of the momentum and test the market. You get an offer that would net you $50 million personally if you sold for all cash. But instead, you roll 20% of the purchase price into equity. The acquiring company sells itself four years later, and your equity value increases by 4x. Looking back, you’ve received two $40 million checks.

Neither outcome is guaranteed, but both have happened. With a strong M&A process, you might get enough leverage to negotiate the structure you want.

Multiple factors influence your M&A transaction considerations. This article outlines a few of those considerations then walks through the details of an equity rollover.

Questions to ask yourself

Why are you selling your business?

Before optimizing the money you get from a deal, consider your motives. Do you want to retire and spend time with family or other activities? Do you see potential for growth within a larger platform? Do you like running the business but want to take some chips off the table?

Everyone has their own reason for selling their business. You can read others’ stories, but your reason will be your own. Only you can decide when to kick off a sale process.

Where are you going? Where is the money going?

Imagine two scenarios.

- Scenario 1: You sell 60% of your business to a private equity fund. You remain the CEO. You take $1m, but the rest of the cash from the deal goes to the company. You hire the COO and VP of Sales to manage the increased demand. You plan to grow the business for 3-5 years and then cash out.

- Scenario 2: you sell 100% of your business to a large public company. You agree to help integrate your team. You’ll be out of the business within 12 months. This is the “big deal” for you: all of the proceeds go to you and your employees who owned the business.

Both of these scenarios involve selling your company. But that’s where the similarities end.

Depending on your goals, you’ll want cash, equity, or something else. If you sell to Google, an equity rollover isn’t likely to go to zero. (Plus, they have a lot of cash to pay you.) You’ll likely have a high salary and a cushy job. This is different from selling to a high-flying startup where you’ll be joining as an executive with a small chance of a large outcome if the company does well.

What’s the cash for? What’s your risk tolerance?

When you sell your company for cash, complete diligence and sign documents, you’ll get a wire transfer for (hopefully) a lot of money. After fielding calls from wealth managers, you’ll realize you have a new problem: how can I grow (and avoid losing) this wealth I just created?

This isn’t financial advice, but after buying a new house and investing in the stock market, what are your other options? Sometimes allocating 10-20% of your wealth to a high-potential, albeit risky, company might be the best choice.

This is exactly what happens with an equity rollover. Instead of an all-cash transaction, you might take 80% in cash and 20% in stock. This provides a cash cushion for your hard work, but also gives you some upside (this is especially exciting if you believe your company can grow with the new owner).

Of course, personal risk tolerance, stage of life, family situation, and existing financial position impact deal structure. Consider if the upside would change your lifestyle, and if the risk is worth taking.

Who is buying the business?

If you do decide you want other consideration (like an equity rollover), the big question is: what are the prospects of that company? This determines the equity’s value.

The answer to this question is both general and specific. It’s general because buyer categories follow similar patterns in reliability, deal structure, and closing speed. For example, selling to Google is a lot different than selling to a small holding company.

There are many differences in how different buyers approach your business. But for this article, I want to focus on the equity prospects if you structure the deal with an equity rollover.

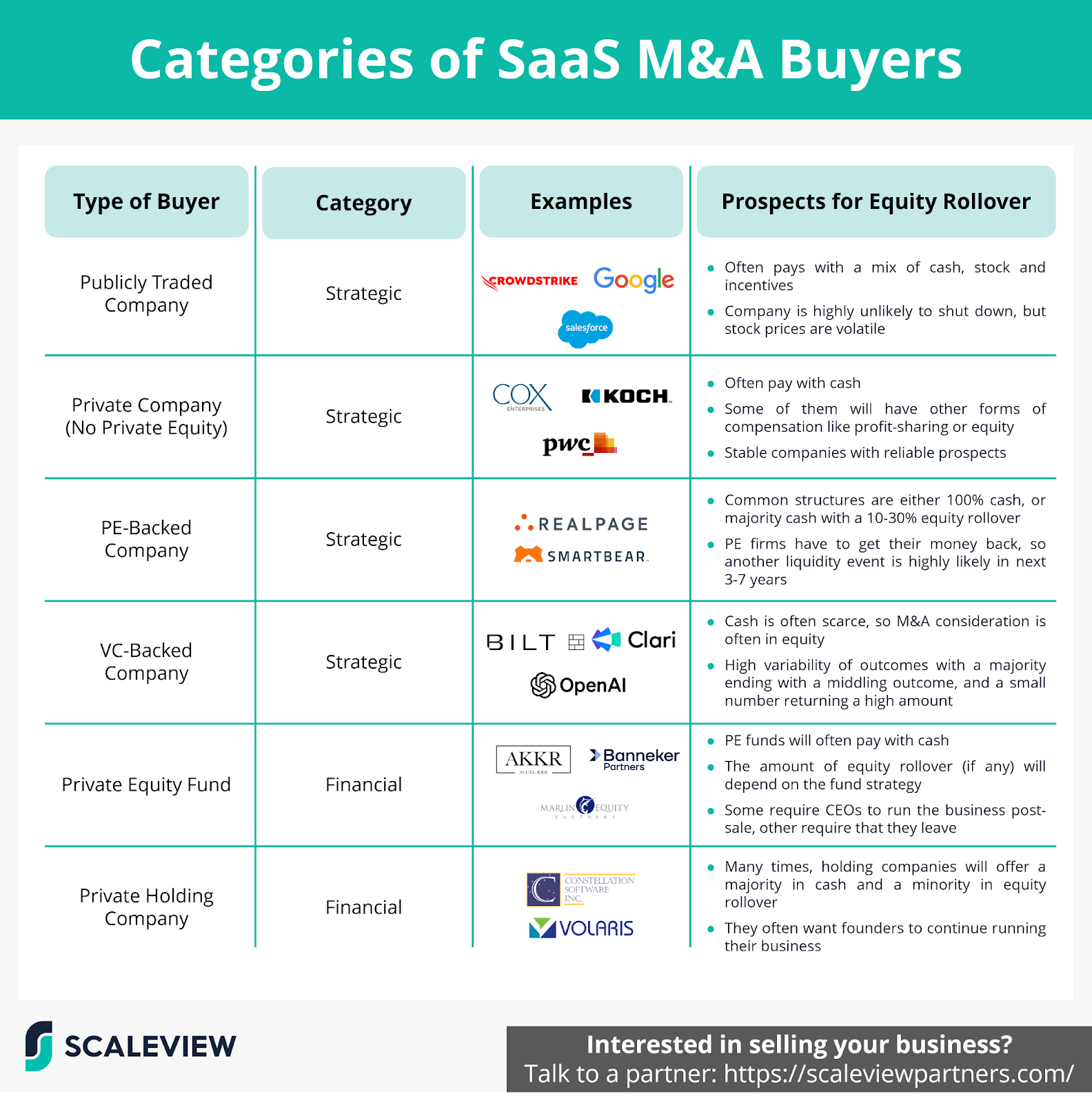

For SaaS businesses with $5-30m in ARR, these are the common acquirer categories and prospects for an equity rollover.

If you exit a small SaaS business, there are a few categories of buyers.

On the strategic side, there are public and private companies. These are big, slow entities that are very stable. If they are public, you can look at their financials, strategy, stock price, etc. and decide if you want to be part of them. Private companies offer stability, but their equity is less liquid (i.e., there are fewer opportunities to sell your shares).

There’s a big section of strategic buyers with institutional capital, either venture capital or private equity. The difference is important! “Private equity backed strategics” (companies that are owned by a PE fund) are reliable buyers with reasonably low risk equity. They need to exit the business within 3-5 years and almost always earn a return. Rolling your equity into this buyer type can likely earn a return.

Venture-backed companies are much different. They often lack cash and many fail (shutting down with zero equity value). However, there’s a small chance a VC-backed business will achieve its ambition and become a large company.

It’s important to know the buyer category for an equity rollover. But you don’t sell your business to a category; you sell to an individual buyer. Analyzing the equity roll is a very specific task.

Your buyer will have a unique product, customers, and brand unlike any other company. They may or may not have investors or debt. Like fund managers, you’ll need to evaluate the investment.

This analysis matters. Think of it as diligence on a multi-million dollar investment because, well, it is. The buyer will ask you a bunch of questions, but you should do the same.

Details about equity rollover

Types of non-cash consideration

Throughout this article, I’ve been using the term “equity rollover” as the main type of payment that isn’t cash. This is true – equity rollovers are common – but it’s just one of a few different types of consideration that can be included in deals. Here’s an overview:

- Equity rollover. The technical definition of an equity rollover is when equity holders in the target company roll a portion of their ownership into the new capital structure as equity instead of cash.

- Earn out. An earn out is like an equity rollover, but instead of taking equity in the new company, you agree to conditions for further payouts. Sometimes these conditions are connected to the acquiring company’s performance (e.g., total revenue) or the target company’s performance within the larger business (e.g., the profit of the target business, now a division of the acquiring business).

- Seller note. A seller note is a loan issued by the seller to the buyer during a transaction. It’s most often used in smaller deals to cover the difference between the buyer’s capital (usually a mix of debt and equity) and the seller’s valuation. It typically has interest and principal payments. It sits higher in the capital structure than equity (or an earnout), ensuring priority repayment in bankruptcy.

Why would a buyer offer non-cash consideration?

There are two parties in a transaction. While fair deals exist, one side usually benefits more. Why would a buyer offer anything other than cash if it benefits you?

The most common answer: cash is king. Liquidity can be used for investing in growth or buying other companies. This is particularly important during tougher economic times or if the buyer has limited cash reserves.

Lawyers view the cash issue differently: an earn-out solves a valuation gap, while an equity rollover addresses a funding gap. Remember: an earn-out is a payment based on future performance. If you believe your business is worth $100m, but the buyer disagrees at $95m, an earn-out lets you “prove” your business’s worth. This is especially important if the buyer is concerned about its future profitability.

They say an equity rollover is used to solve a funding gap due to the way private equity funds model their investments. They focus on the cash invested in a business, the cash received when they sell it, and the time it takes to do so. By using a rollover, they can invest less cash in the acquisition at the start.

Beyond the cash constraint, buyers also like to add non-cash consideration to reduce risk and align incentives. Perhaps they want the management team to run the business after the acquisition. An equity rollover might be the best way to motivate them. Alternatively, if the buyer is unsure if the seller can reach certain milestones, an earnout can incentivize them and avoid overpaying if they don’t come to fruition.

Key terms

While I highly recommend hiring a lawyer for your transaction, it’s useful for you to know the key terms before negotiating.

Earnout key terms:

- Time Period. This is the duration that the financial or performance goals must be achieved to trigger the payments. It commonly spans from one to several years.

- Performance Milestones. These are the defined financial targets or KPIs that must be met to qualify for earnout payments. Examples include reaching specified revenue levels, number of users, or EBITDA targets. This may be a chance to get creative by aligning your interests with the buyers.

- Escrow Account. This is a secure account where part of the purchase price is held until the seller meets the earnout criteria. It ensures the buyer has the money to pay the consideration but the seller doesn’t have it until they meet the criteria.

- Clawback Provision. A clause that allows the buyer to reclaim part of the earnout payment if conditions aren’t met or discrepancies are found post-deal. Watch out for this provision and review with your lawyer.

Key terms for equity rollovers:

- Equity Rollover Percent & Amount. The percent & amount of equity in the merged or acquiring entity.

- Vesting Schedule. The criteria dictating when the seller fully acquires ownership of the rolled-over equity. You might receive all of the equity during the transaction, but it might only become yours after a time period (or occasionally performance milestones).

- Lock-Up Period. A mandatory time frame where sellers can’t sell their newly acquired shares. This is common for both publicly traded and private buyers.

- Tag-Along Rights. These provisions allow you (which will be minority shareholders) to exit alongside a majority seller under similar terms. It ensures you get the same deal as the buyer when the acquiring company sells the whole business after a few years.

Final note

An equity rollover is just one component of the decision to sell your business. Consider your goals and your lifestyle. It’s a big decision and not one to take lightly.

Whether you stay with the acquiring company or not, non-cash consideration could be a large part of the deal you end up taking. If you sell your business, know the tradeoffs between the types of non-cash consideration and the buyer you’ll hold equity in.

Talk to friends who have gone through it and consider hiring an investment banker (this is something we do at ScaleView!) and a lawyer to help you through the process.

Cash is crucial for a deal. I hope this article showed you there are other forms of consideration to think about as well.