Popularized by venture capitalist Brad Feld, the Rule of 40 describes a benchmark metric popular among SaaS founders and investors. The Rule of 40 states that your growth rate and your profit margin should add up to at least 40%. In the context of the original blog post, 40% marked a “healthy SaaS company” that’s able to raise capital. If you are growing at 20%, Brad Feld says, you should be targeting a profit margin of 20%. As much as the calculation of the Rule of 40 metric seems simple on the surface, it masks a host of nuances that offer useful levers we think every successful SaaS operator should have in their toolbox.

As a financial metric, the Rule of 40 reflects the tradeoff between growth and profitability that every SaaS operator faces. As businesses grow larger, a higher base effect translates into lower growth rates – the more revenue you have, the more it takes to increase the same on a percentage basis. At scale, software businesses also often generate higher margins. Once a software company matures, they typically spend less on both product development and sales – increasing their margins in the process. An example of this is Oracle. Oracle tripled its revenue during 2005-2011 with EBITDA margins in low double digits. Much recently, however, the storied computer software firm has seen anemic growth during 2012-2022, often growing at low single digits with ~40% EBITDA margins.

The Rule of 40 establishes an acceptable threshold on the balance between how much the business needs to grow and their profitability. A fast-growing SaaS company needs to make sure the expansion efforts do not outstrip its ability to manage its costs. For most SaaS companies, incentive plans for the sales team, product development costs, and advertising expenses to acquire new users and keep the existing user churn low eat up a disproportionate amount of cash. More growth is always better, but the growth decay over time should track margin expansion as the SaaS business becomes more mature.

The 40% benchmark of the rule is not set in stone, but rather swings like a pendulum depending on the investor appetite, market conditions, and cyclicality. During times of excess exuberance or investor despair, the market-observed metric may converge to 60% or 20%, respectively, to set the floor for a SaaS financial profile. Despite its vagaries, the benchmark has proven useful for SaaS operators. Benchmarking allows operators to compare how the combination of growth and profitability maps into the valuation, often expressed in terms of Enterprise Value to Sales (EV/Sales), and track their progress as the business crosses the pre-set milestones.

In the end, it is one of a dozen useful measures that should be used by savvy tech operators. You can leverage it to do back-of-the-envelope calculations and make informed and prompt decisions in the fast-paced SaaS world.

In the following article, we break down the formula, illustrate the calculation behind this much-discussed metric, and bring it to life with real-world examples from the SaaS landscape.

Rule of 40 Formula

Simply, the formula for the Rule of 40 is taking the sum of a growth metric and a profitability metric. The sum of 20% growth and 20% profitability equals a 40% Rule of 40.

Despite it’s simplicity, there is no definitive consensus on which growth and profitability metrics to use when calculating the Rule of 40. This makes it hard to use to compare between different SaaS companies. Operators have a slew of options to pick from as proxies for growth and profitability.

On the former, the Rule of 40 metric incorporates a top-line growth metric such as year-over-year (YoY) or quarter-over-quarter (QoQ) revenue, annual recurring revenue (ARR), or monthly recurring revenue (MRR) growth. Although the choice of a time period and metric can be subjective, operators should parse through the velocity of growth and current business profile to choose one that most accurately represents the quality of their revenue growth (not necessarily that just paints the business in the best light). For example, MRR or ARR may be preferable because it excludes one-time service revenues, but GAAP revenue may be more useful in standardizing the measure across a broad set of business models.

On the profitability side of the equation, the margins can be any of EBITDA, EBIT, free cash flow (FCF), Net Income, or Cash Flow from Operations (or something else entirely). The best metric hinges on the business model, financial profile, and what you (or your board or investors) care most about. Here, the questions revolve around what expense items are significant and need to be normalized to allow for an apples-to-apples comparison. For example, running a SaaS business on proprietary infrastructure instead of an off-the-shelf cloud provider will create material differences between EBITDA and FCF because of the cash and accounting effects of equipment purchases, lease costs, and debt to finance the investments.

Sample Calculation: Adobe

To understand the Rule of 40 more concretely, we’ll walk through an example calculation using public software company Adobe.

Adobe is a $220B+ market cap SaaS company that provides a cloud-based software product suite aimed at maximizing team efficiency. Their product suite includes some software that you might be familiar with: Acrobat (PDF solution), Photoshop (editing and creating images), Illustrator (Creating vector art and illustrations), and Firefly (multimedia created via Generative AI). Please note that in the following set of calculations, we are using YoY quarterly revenue growth and quarterly EBITDA margin. We also round the percentages to two decimals for intermediate calculations.

For the growth side of the equation, we will use the FY2023 Q3 and 2022 Q3 GAAP revenue numbers from Adobe’s latest quarterly filing to calculate the YoY quarterly growth at Adobe.

Calculation: $4,890 / $4,433 = 10.31% revenue growth

For the profitability side of the equation, we will look at the FY2023 Q3 EBITDA margin. Since Adobe does not report EBITDA figures, we will calculate it based on the publicly available information.

Step 1: EBITDA = EBIT + Depreciation and Amortization

Calculation 1: $1,697 + $218 = $1,915 million EBITDA

Step 2: EBITDA margin = EBITDA / Revenue

Calculation 2: $1,915 / $4,890 = 39.16% EBITDA margin

To reflect a better picture of the normalized business performance, we could go even further to make adjustments to the EBITDA figure by accounting for stock-based compensation and acquisition-related expenses [1]. Even though it might paint a more accurate picture, for simplicity we will stick with the standard EBITDA margin figure calculated on an unadjusted basis for the Adobe example[2].

Lastly, we combine the two figures above to arrive at the Rule of 40 metrics:

Formula: “Rule of 40” = YoY quarterly revenue growth + quarterly EBITDA margin

Calculation: 10.31% + 39.16% = 49.47% Rule of 40

Despite being a mature SaaS company with low double digit revenue growth, Adobe boasts a high profitability margin on an EBITDA basis. As dictated by Rule of 40, this should give Adobe a premium valuation as it comfortably passes the 40% threshold.

Indeed, it does. Based on an Enterprise Value as of September 28 close of $229.99 billion and LTM sales of $18.89 billion, Adobe’s LTM EV/Sales multiple is a whopping 12.2x, on the upper side of 9.3x SaaS EV/Revenue multiple average according to the quarterly SaaS update published by the ScaleView team.

Public Comps Benchmarking

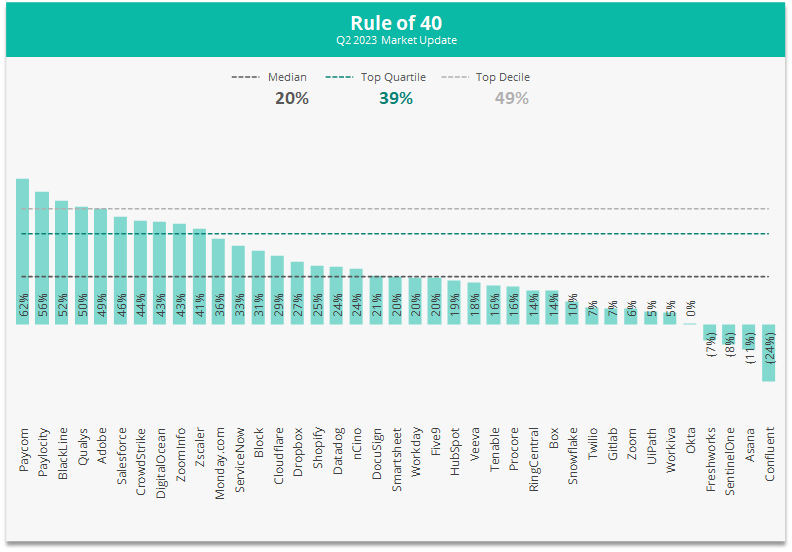

One way to better understand the Rule of 40 metric is to study public market data. Here’s a chart of X public SaaS companies and their respective Rule of 40 from Q2 2023:

To highlight the variability of the metric across SaaS businesses, we’ll walkthrough examples of Salesforce, Paycom, and Workiva and why they are different.

Salesforce: Rule of 40 = 46%.

Takeaway: cost cutting can improve both Rule of 40 and EV/Sales multiple.

In February 2023, Salesforce faced backlash from a group of activist investors to prioritize profitability over growth in a slow tech spending environment. They were trading at a rock-bottom 3.92x EV to Forward Revenue multiple and their revenue growth stalled from ~25% from 2019 to 2022 to below 20% in 2023 (lowering the Rule of 40 in the process).

During the FY2024 Q1 earnings call, Mark Benioff emphasized the pivot to cost-cutting and said that they would trim expenditures on discretionary items such as supplementary employee benefits. The EBITDA margin has since recovered to ~20% on an LTM basis as of July 2023 from 14.18% FY2023 EBITDA margin, offsetting the revenue slowdown and increasing the Rule of 40 back above 40%.

In lockstep with this move to prop up profitability, Salesforce’s EV to Forward Revenue multiple recovered to 5.12x as of October 2, 2023. We can expect Salesforce to continue this path: cut costs and improve profitability as growth slows.

Paycom: Rule of 40 = 62%.

Takeaway: capital efficient, bootstrapped DNA can lead to high Rule of 40.

Provider of online payroll services and HR software solutions with a focus on SMB, Paycom boasts both high growth and profitability resulting in a Rule of 40 of 62% — the highest in our analysis. While there are certainly many reasons why they are one of the best software businesses, Paycom had no traditional VC fundraising round which forced them to come up with efficient go-to-market strategies.

As with many SMB-focused bootstrapped companies (such as Mailchimp), Paycom’s efficient go-to-market approach in the enabled rapid growth while keeping costs low. First, Paycom was one of the early company to use product-led growth, providing value to customers without a salesperson and using an automated funnel to make the sale. Additionally, Paycom’s salesforce was trained to define customer needs prior to talking to them. In addition, they kicked off targeted partnerships—brand partners include SharkTank co-host Barbara Corcoran!—and gave to charities to increase brand awareness. The virtuous growth cycle asserted itself as their customer’s scale: the customer grows their business, and with the growth required more services. Paycom could expand many of their customers leading to upsells and increasing average contract sizes.

With an LTM S&M margin at a respectable 25% (compared to an industry median of 41%) and R&D-lite HR solutions, Paycom is well positioned to further penetrate the enterprise HR solutions. A tale of Rule of 40 managed right, Paycom commands a premium 9.25x Enterprise Value to Sales multiple, according to Pitchbook.

Workiva: Rule of 40 = 5%.

Takeaway: revenue and profitability forecasts can be as important as the current metrics.

Workiva is a software company that makes a cloud-based financial reporting software product. The product integrates data from ERP, HCM, CRM systems, and other sources and dramatically simplifies the otherwise-complex financial reporting process. They were founded in 2008 and have grown to almost $600m in revenue.

While Workiva’s Rule of 40 is a paltry 5% (which is the same it was five years ago), they trade at a relatively high 9.12 Enterprise Value to Sales multiple. The key reason? Forecasts.

Financial reporting is a very large market, estimated at $16B, and Workiva management, investors and research analysts all anticipate continued ~20% year-over-year revenue growth. Additionally, private equity firms think Workiva can maintain that growth while improving their currently negative EBITDA margins. In fact, in September 2022, the rumor spread that TPG and Thoma Bravo (two very active software private equity funds) would take Workiva private at a $3.4 billion valuation. The deal has since been canceled, but the public markets agree that margins can be improved.

All in all, Workiva is currently getting the valuation benefits of a positive future forecast. We’ll have to see if their operations can justify it over the coming years.

Final Takeaways

The Rule of 40 is useful because it’s shorthand for business health and correlates with valuation. It forces disciplines on operators not to be skewed heavily either towards profitability or growth. It bridges the gap between the two of the most oft-cited business metrics and sums it up in one figure that enables the operators—who often rely on qualitative measures of the company or team performance rather than financial engineering—to come up with a high-level view of the company’s track record. More growth is always better, but the growth decay over time should track margin expansion as the SaaS business becomes more mature. This makes the Rule of 40 useful for any software business: big or small, new or old, bootstrapped or venture-backed, public or private.

40% might be the right Rule of 40 number, but it also might not. There are questions about whether 40% is the right benchmark. The metric is driven by business cycles, interest rates, economic growth, capital market optimism, and the funding strategies. The acceptable threshold may swing depending on investor expectations.