Marketing software unicorn Klaviyo went public last week at a $9.2B valuation. This is big news: it’s the first large, high-quality software business to go public since the market cooled off in 2021.

While there have been several summaries of the S-1 already published, here at ScaleView Partners, we get a lot of questions from software CEOs asking our advice about the software market, strategic initiatives, and broader capital markets strategy. We figured this IPO would be a good opportunity to discuss what operators can learn from Klaviyo’s IPO.

Before we get too far into the analysis, let’s set the stage by going over a few highlights of Klaviyo’s business:

- Klaviyo is a marketing automation tool that covers email, SMS, mobile push and reviews, and they primarily serve small and medium-sized businesses (SMBs).

- They had $585m revenue in the last twelve months at a 57% growth rate.

- They have 130k customers with an average contact value of ~$5k.

- Klaviyo has a 75% GAAP gross margin.

- During the first 6 months of 2023, Klaviyo had positive Net Income. This is one of the very few software IPOs that had positive Net Income at IPO.

- Klavyio only used $15m of the $454.8M that they raised.

In this piece we want to discuss two things that stood out for us: how was Klaviyo so capital efficient, and how will investors value Klaviyo’s business?

In the first section, we’ll talk about what capital efficiency means, why software companies are capital efficient and why Klaviyo was best-of-breed even compared to other software companies.

In the latter section, we’ll dive into valuation. Using a public comparables analysis, we’ll benchmark Klaviyo against its publicly traded peers as an example of how an investor might benchmark your company. For example, Klaviyo is growing faster than most other public software companies that sell into SMBs. Why is this the case and how does it impact valuations? If you ran a software business, how would it impact your valuation if you were growing faster or slower than peers?

Let’s get into it.

Capital Efficiency

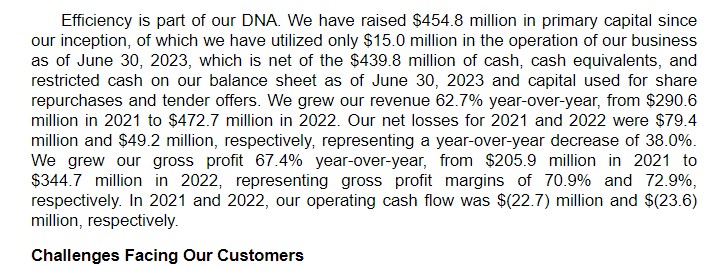

Klaviyo has only burned $15m of cash from the time of inception to the time of IPO. This is one of the most capital efficient businesses to ever IPO, even among software companies. How did they do it and what principles can other software founders learn from them?

First of all, what are we saying when we say, “capital efficiency”? Capital efficiency can be defined in many ways, but one of the simplest ways is the amount of cash that the business spent that it didn’t generate with its own business operations. In other words, if you take the total amount of cash raised, and remove the amount of cash that’s left on the balance sheet, how much did they spend? Despite raising over $450m, Klaviyo only burned about $15m:

Source: Klaviyo Form S-1(1)

Capital efficiency fosters wealth creation by allowing you to own more of your business.

It’s more lucrative for founders and existing shareholders to own a business that’s capital efficient. This is because you gain leverage in your capital markets decisions. For simplicity, compare two businesses: one is cash flow positive, one is cash flow negative. Both have large ambitions and want to grow quickly. The cash flow positive business has much more negotiating leverage with investors compared to the cash flow negative business. They can keep functioning without the investors’ capital!

Tactically, this means the business that’s more capital efficient gets better deals terms and/or a higher valuation when raising money. This is important. It’s easy to intuitively think, “higher valuation = better”, but it shows up quite tangibly during a liquidity event like Klaviyo’s IPO. We can see exactly how much of the business the founders sold, how much they still own, and how much it’s worth.

At IPO, Klaviyo founder Andrew Bialecki owned 38.1% of Klaviyo. At an $9.2B market cap (307.9 million fully shares outstanding multiplied by the $30.00 per share IPO price), this means his personal stake in the business is worth $3.5B. This personal ownership is much higher than average: according to a 2022 IPO analysis, the average founder ownership across 198 companies was 20% and the median was 15%. If the Bialecki had been diluted according to the average amount, he would have $1.7B less in personal value.

Klaviyo is capital efficient because it’s a software company.

The next obvious question: if capital efficiency is so important, how did Klaviyo build such a capital efficient business? Part of the answer is because Klaviyo is a software company.

Software is one of the best business models. You make your product once and you can sell it as many times as you like with very little additional cost. This property – called low incremental fixed cost – shows up on the income statement in the form of 70-90% gross margins. Compare this to other industries that often hover around 20-50% gross margins and it’s easy to see why it’s great to be in the software business.

The high gross margins isn’t the only reason why software businesses are capital efficient. Another benefit of software businesses is the contract structure. The most common business model for software these days is software-as-a-service. This is where your customer sign a contract and receive access to your software for a period of time (typically a month or a year).

There are two features of SaaS contracts that really matter for capital efficiency: pre-payment, and contractually recurring. SaaS contracts often are pre-paid, meaning the customer pays you at the beginning of the contract and uses the service over the course of the contract. You get the cash before providing the service! And that capital can be funneled into building new products or acquiring customers.

The other component is the contractually recurring nature of their contracts. This means that contracts new automatically months or year in case of long-term contracts. This not only provides for predictable stream of revenue and stable customer relationships for you, but it also aligns incentives with your customer as you want to keep them satisfied with new updates.

Klaviyo is also capital efficient because of specific initiatives, strategies and metrics.

Building software is a good choice for an entrepreneur looking to build a valuable business, but even compared to its’ software peers Klaviyo is capital efficient. They are performing above other software businesses.

This is due to their unique initiatives, strategies and metrics as a business. A few things stood out in our research:

- Klaviyo Attributed Value

- Third-party distribution through Shopify

- An incredibly easy-to-use product.

The first thing Klaviyo did was create their own metric for how they provide value to their customers. It’s called. Klaviyo Attributed Value (KAV) and it’s a customer ROI metric designed to track the value generation attributable to the company’s marketing automation engine. Specifically, it refers to the amount of revenue Klaviyo customers generated within a specific period of time after the marketing campaign was sent (24 hours for SMS and 5 days for email).

Reporting of KAV incentivizes Klaviyo to drive higher sales, conversion, and traffic for its 130k+ member customer base through effective marketing outreach. The KAV metric directly hits at the effectiveness and attributability of a marketing campaign. It aligns the interests of Klaviyo and its customers as the its customer base’s success in achieving higher sales and traffic is directly correlated with Klaviyo’s ability to scale.

Second, Klaviyo benefited from a long-term and multi-faceted partnership with Shopify. Klaviyo first officially became part of the Shopify Web App Store in 2017. In addition to being on the Shopify Web App Store, in 2022 Klaviyo and Shopify entered into a strategic partnership where Klaviyo received a $100m investment from Shopify in exchange for Klaviyo being the official recommended email provider on Shopify Plus. The current term for this partnership is 2029 and on-going year-by-year after that.

Source: Klaviyo website

Source: Klaviyo website

Partnering with Shopify has many benefits, the most obvious one being cheaper customer acquisition. Shopify’s growth over the past decade is staggering. In 2022, Shopify posted $5.6 billion in revenue, increasing by more than $4 billion since 2015. This includes a now 5,300 merchants using Shopify Plus (available to merchants with $1m-$500m revenues). Even though the ecommerce trends cooled off as the world resumed in-person activities after the pandemic waned, Shopify continues to be a linchpin in the e-commerce space and continues to grab market share with double-digit sales growth.

Valuation & Public Comps

As mentioned, Klaviyo is the first major public software company to go public since the technology market bubble started bursting at the end of 2021. This has a few takeaways: first, it will be interesting to see how Klaviyo trades once it’s on the open market. As of their IPO on September 20th, their share price was $30. This translates to a ~$8.2B valuation (or ~14.1x LTM revenue). This is lower than their last private market fundraise (valuing them at $9.5B) but not too much of a haircut given the changes in the macro environment.

For valuation and benchmarking in the public markets, there’s a few ways to position Klaviyo. We split the public comps analysis into three buckets: SMB end-market, large cap competitors, and high-growth SaaS.

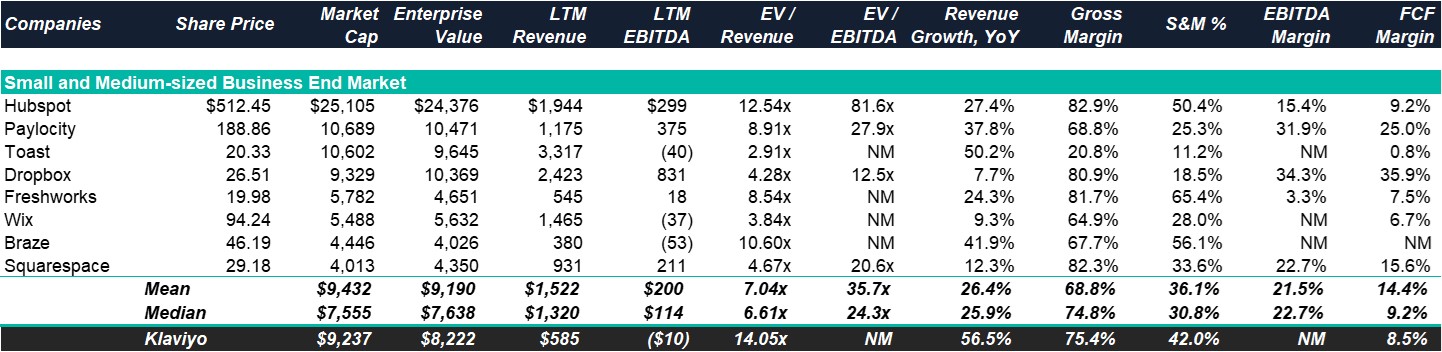

SMB End-Market

The SMB end-market was the first thing bucket that Klaviyo falls into. While they are moving up-market, Klaviyo’s customer base started with SMBs and is still primarily SMBs. They have 130k customers.

This makes sense as a comparables set because this end market typically has different operating dynamics than enterprise end markets. From a go-to-market perspective, SMBs tend to find products through channels like search engines or referrals from other business owners. There isn’t typically a request-for-proposal (RFP) process or a long, multi-month sales cycle like there is in the enterprise market. Easy and intuitive onboarding is critical for SMBs as the sales process doesn’t typically involve live demos or a hand-held implementation process. Relatedly, products built for SMBs are typically easier to use than products for enterprise. For example, products for SMBs might automate analytics, providing a pre-generated dashboard, while a similar product for the enterprise would have more customization options (and would be used by the enterprise who has data engineers who can build data pipelines and visualizations for non-technical users).

For this comps analysis, we selected other public software companies that served a large SMB base (or, at least began their journey serving that market).

A few key takeaways from the SMB end market analysis:

- Klaviyo is growing faster than every other SMB public comp in this data set. The average and median is in the mid-20s while Klaviyo grew 56.5% year-over-year.

- The larger companies on this list are 3-6x large (in terms of revenue) than Klaviyo. Some of them – like Wix – have similar-looking end markets, implying that the total addressable market (TAM) for Klaviyo likely won’t be a limiting factor anytime soon.

- With higher growth and a similar gross margin profile, we expect Klaviyo to trade significantly better than this set of companies. Removing Toast (20% gross margin), the market is rewarding profitable growers: the fastest growing companies are Braze (41.9%) and Paylocity (37.8%) and both are trading above the mean/median at 11.2x and 9.5x EV/Revenue respectively.

Large cap

Klaviyo can also be compared to large cap companies that sell a competing or similar product. These businesses might get more of their revenue from the enterprise customer segment, but these companies offer similar marketing technology products. They ended up as large-cap companies because they either were direct marketing technology competitors or they focused on a similar SMB eCommerce end market (or both).

A few key takeaways from the large cap software analysis:

- Large cap companies in this set are trading at a higher revenue multiple on average than businesses focused on SMB end markets. The mean is 10.4x compared to 7.0x and the median is 10.9x compared to 6.6x. A natural conclusion might be that the market appreciates larger companies by default, but looking a layer deeper we find that the EBITDA margins are much higher for this group of large cap companies compared to the first comp set. This isn’t terribly unsurprising as companies often shift from higher growth to higher profitability as they move along the S-curve.

- Not only are their EBITDA margins higher, but they’ve also started generating serious free cash flow as Salesforce, Adobe and Intuit all post higher than 30% FCF margins. This is also much higher than Klavyio’s FCF margin.

- The smallest company in this group is Shopify at a ~$84B market cap and ~$6B in revenue. The other companies are multiples larger than that. While it’s important to compare these companies to Klaviyo because they have similar products, the business fundamentals are quite different.

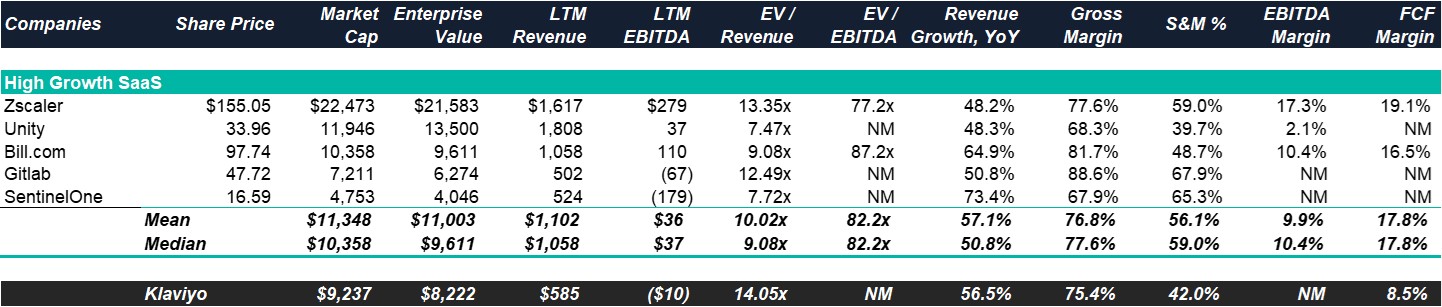

High-Growth SaaS

The final comp set for Klaviyo is a more generalized group of high-growth software companies. At 56.5% year-over-year revenue growth, Klaviyo is on par with the top decile software growers and we wanted to see how it compared.

A few key takeaways from the high-growth SaaS analysis:

- From a financial perspective, this comp set looks the most like Klaviyo. The revenue growth and gross margins are on par with Klaviyo. A few of the companies are similar size and a few are a bit larger. A few of the companies have negative EBITDA and a few have positive. All of these are in-line with Klaviyo’s financial profit.

- However, the products and end markets of these companies look very different. Zscaler and SentinelOne are in cybersecurity, Unity is a gaming engine, Bill.com is back-office financial software and Gitlab is a developer platform. None of them have marketing technology products.

- Perhaps a sign of the times, this high-growth SaaS group trades at about the same multiple as the much slower growth large-cap SaaS group. These days the market is rewarding profitability more than growth.

Final Takeaways

With all that said, what can operators thinking about an exit tactically learn from Klaviyo’s IPO?

Capital efficiency can have a material effect on your wealth. While not the only reason to start a company, if you’re thinking about a sale, chances are personal proceeds are one of the most important factors in your decision. Part of this is determined by valuation – we’ll get to that more in a second. But part of it is due to how much of the business that you own. If you build your business in a capital efficient way, you can either own 100% of it yourself or can have increased leverage when you raise a minority round. Regardless of your exact choice, ownership percent shouldn’t be taken lightly and the best way to keep more of your business is to create a good business.

Study the best businesses to learn from their tactics. Early on, Klaviyo focused almost exclusively on the email marketing automation for eCommerce companies in the Shopify ecosystem. This is a very niche area, but it allowed them to piggyback on top of the eCommerce (and Shopify) boom over the last decade. They double downed on the focus by creating a metric – Klaviyo Attributed Value – that aligned them with their customers. Through these strategic decisions (and plenty others that we don’t know about), Klaviyo was able to grow incredibly efficiently.

Valuation is an art, not a science. But some principles still universally apply. Investors will view your business through a number of lenses. We walked through how an investor might think about Klaviyo here: through their end market (SMBs), product (marketing software) or growth profile (high-growth). The art is figuring out how investors will view your business and positioning it in a favorable light. While the only way to truly know how much your business is worth is to have an offer in hand, you can get an estimate based on public market analysis like we did above.